Sound Transit's

Prop 1 in 2008:

$107 Billion Tax

Collection Authorized

by John Niles and

Jim MacIsaac

The public is

hearing two cost numbers for the Sound Transit Proposition 1 tax package on

the November 4, 2008 ballot. The figure Sound Transit is placing on the

November 4 ballot is $17.9 billion in construction costs.

However,

another valid

number for Prop 1 is $107 billion in authorized tax collections (see chart below),

conservatively estimated.

What's the Difference between Cost Estimates and

Authorized Taxes?

Sound

Transit's $17.9 billion represents the estimated cost of construction and

operations of Sound Transit's light rail additions and other services through

the scheduled end of the light rail expansion program in 2023. Sound Transit

will likely sell 30-year bonds through this last year of construction.

The much

larger $107 billion represents the tax collection authority of Sound Transit

through 2053 when the last of its 30 year bonds -- borrowed money to cover

light rail construction costs -- reach their maturity and are paid off.

Sound Transit Taxes are Authorized Forever

Approval of

Sound Transit Prop 1 would authorize extension in full of the Sound Move taxes

authorized in the 1996 vote. These existing taxes were at one time scheduled

to be considered for reduction -- a reduction called "roll back" -- after 2006. But since these existing sales taxes will be

used to secure all Prop 1 construction

bonds, Sound Transit will have legal claim to continue the 1996 sales tax in

full until all the bonds authorized by Prop 1 are paid off in 2053. This is the

scheme by which it secured ongoing authority to collect the Sound Move MVET

(car tabs tax) for 30 years, using this tax as part of the security for a 1999 bond

issuance.

Sound

Transit taxes listed in the Prop 1 authorizing Resolution 2008-11 are not

scheduled to ever end (sunset) since the agency needs the flexibility to keep

collecting them in perpetuity to cover ongoing

operating and maintenance costs, agency administrative costs, and capital replacement reserves.

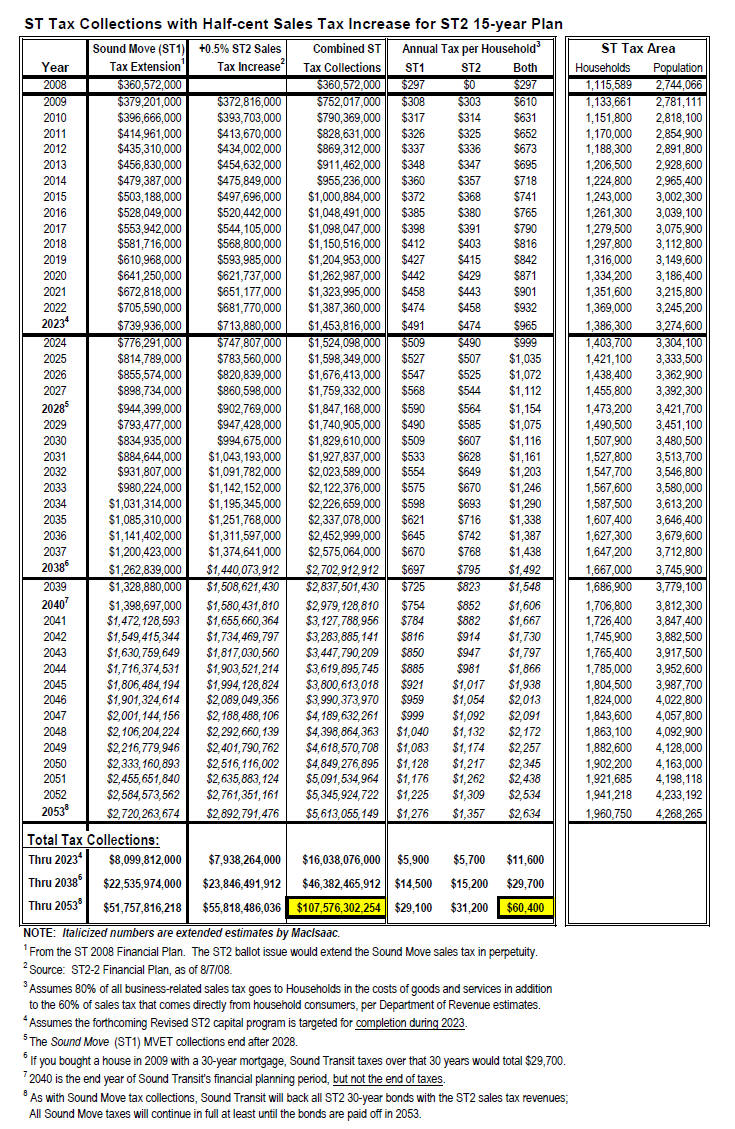

The chart below prepared by Jim MacIsaac shows Sound Transit tax revenues thru 2053

when 30 year bonds sold at the end of the scheduled light rail construction

period would be scheduled to be paid off. Using 2053 as the end date for

calculation of total tax revenue is conservative considering the taxing

authority is in perpetuity. Even Sound Transit's own benefit-cost analysis

shows a financial horizon (end date) of 2063.

What

About the $157 Billion Tax Collections Widely Publicized for Prop 1 in 2007?

In 2007, the

combined Roads & Transit taxes for Prop 1 came out to $157 billion, of which

$141 billion was for Sound Transit and $16 billion was for the RTID road

taxes. Since the sales tax rate in 2008 is still 5/10 of one percent just like in

2007, why isn't $141 billion the number for estimated total tax collections

this year? One reason is that a less positive economic outlook

now has caused Sound Transit to lower its tax revenue forecast, even though

the agency has not stepped back from asking for the same tax rate. The biggest

reason, worth a $25 billion reduction from last year, is that we cut short the

time horizon of our tax collection calculations by four years to reflect the

claimed shorter time period of Sound Transit's construction program in the

2008 version of Prop 1. However, recall that Sound Transit's current

construction schedule to complete Sound Move is more than double the estimate

provided to voters in 1996.

The

45-year estimate of cumulative tax revenues for the Prop 1 package is now

estimated as follows from 2009 thru 2053: